All Categories

Featured

Table of Contents

In addition, as you manage your policy during your lifetime, you'll desire a communicative and transparent insurance policy supplier. In comparison to an entire life insurance coverage plan, universal life insurance supplies adaptable costs payments and tends to be less costly than an entire life policy. The main negative aspects of global life insurance policy plans are that they need maintenance, as you need to keep track of your plan's cash worth.

Accumulation Value Life Insurance

Neither entire life or universal life insurance policy is better than the other. Universal life insurance may attract those seeking irreversible insurance coverage with flexibility and greater returns.

Monetary strength and consumer contentment are hallmarks of a reputable life insurance company. Monetary strength demonstrates the capacity of a company to withstand any kind of economic circumstance, like an economic crisis.

On top of that, the research shows market standards, indicating which companies drop above and below sector averages. Accessibility is additionally a primary aspect we take a look at when evaluating life insurance policy companies. Accessibility describes a policy's affordability and addition of those in various risk courses (health classifications, age, way of lives, etc). No business wishes to transform away sales, in theory. new york universal life insurance.

We utilize a company's website to review the expansiveness of its product line. Some business provide an extensive listing of long-term and short-term policies, while others only give term life insurance policy.

Universal Term Life Insurance

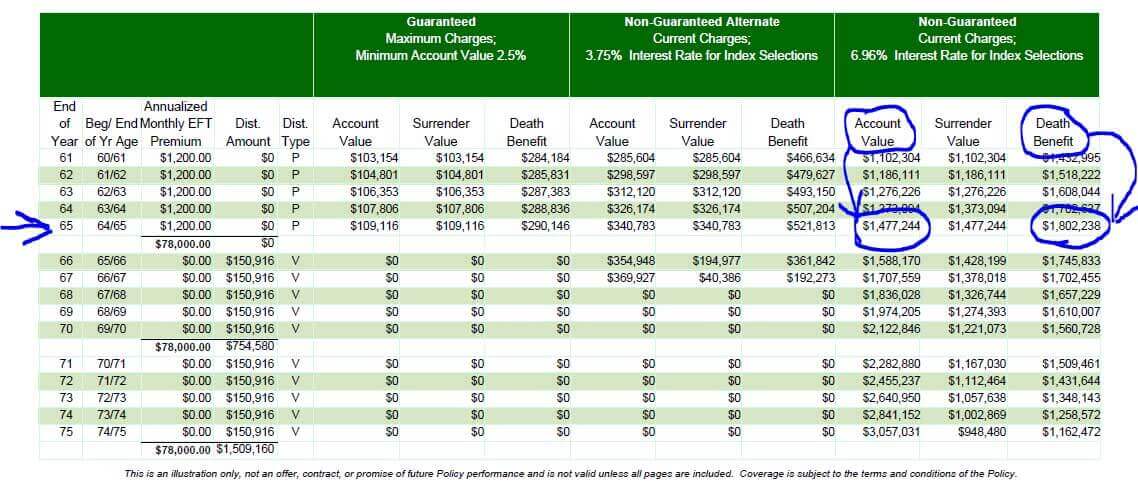

If your IUL plan has adequate cash money value, you can borrow against it with versatile repayment terms and low rate of interest. The choice to develop an IUL plan that shows your certain demands and scenario. With an indexed universal life plan, you assign premium to an Indexed Account, therefore developing a Sector and the 12-month Section Term for that segment begins.

Withdrawals may happen. At the end of the segment term, each section gains an Indexed Credit report. The Indexed Debt is calculated from the change of the S&P 500 * during that one- year duration and goes through the limitations proclaimed for that sector. An Indexed Credit score is computed for a section if value remains in the sector at sector maturation.

These limitations are figured out at the beginning of the segment term and are guaranteed for the entire segment term. There are four options of Indexed Accounts (Indexed Account A, B, C, and E) and each has a different sort of limitation. Indexed Account An establishes a cap on the Indexed Credit for a segment.

Iul Vs 401k Calculator

The development cap will certainly vary and be reset at the beginning of a segment term. The participation rate identifies exactly how much of a boost in the S&P 500's * Index Value puts on sections in Indexed Account B. Greater minimal development cap than Indexed Account A and an Indexed Account Charge.

There is an Indexed Account Fee linked with the Indexed Account Multiplier. Regardless of which Indexed Account you pick, your cash money value is always safeguarded from negative market efficiency. Cash is transferred at the very least as soon as per quarter right into an Indexed Account. The day on which that occurs is called a sweep day, and this produces a Segment.

At Segment Maturity an Indexed Credit history is computed from the adjustment in the S&P 500 *. The value in the Segment gains an Indexed Credit scores which is calculated from an Index Development Price. That growth rate is a percentage adjustment in the current index from the beginning of a Section till the Segment Maturity date.

Segments automatically renew for one more Section Term unless a transfer is asked for. Costs got considering that the last sweep day and any asked for transfers are rolled right into the exact same Sector so that for any kind of month, there will certainly be a single brand-new Segment developed for an offered Indexed Account.

Here's a little refresher course for you on what makes an IUL insurance coverage various from various other kinds of life insurance policy products: This is permanent life insurance, which is essential for firms that watch out for tackling more threat. This is because the policyholder will certainly have the coverage for their whole life as it builds cash value.

Vul Vs Iul

Rate of interest is earned by tracking a team of supplies picked by the insurer. Threat assessment is an important component of balancing value for the customer without threatening the business's success through the survivor benefit. On the various other hand, most various other kinds of insurance coverage just expand their cash money value via non-equity index accounts.

Policies in this group still have cash worth development more dependably because they build up an interest rate on an established timetable, making it simpler to manage risk. Among the more adaptable choices, this option is possibly the riskiest for both the insurance provider and policyholder. Stock performance figures out success for both the company and the client with index global life insurance policy.

While supplies are up, the insurance coverage plan would execute well for the insurance policy holder, yet insurance providers need to regularly examine in with danger assessment. Historically, this threat has actually paid off for insurance policy firms, with it being one of the industry's most profitable sectors.

For insurance firms, it's extremely essential to divulge that risk; customer connections based upon depend on and dependability will assist the company continue to be successful for longer, even if that firm prevents a short windfall. IUL insurance coverage might not be for everybody to construct value, and insurance providers need to note this to their clients.

Universal Life Insurance For Retirement Income

For instance, when the index is performing well the value skyrockets past most other life insurance policy plans. Yet if we take an appearance at the plummeting market in 2020, indexed life insurance policy did not boost in policy value. This positions a threat to the insurer and especially to the policyholder.

In this situation, the insurance company would certainly still get the costs for the year, however the bottom line would certainly be higher than if the proprietor maintained their plan. If the market tanks, some firms use an assured price of growth which could be high-risk for the insurance provider. Insurance coverage business and those that work in the industry need to be knowledgeable about the Dodd-Frank Wall Road Reform and Consumer Protection Act, which exempts an IUL insurance plan from comparable federal guidelines for stocks and alternatives.

Insurance representatives are not financiers and should discuss that the policy needs to not be treated as a financial investment. This develops client trust fund, commitment and contentment. Concerning 52% of Americans live insurance coverage according to LIMRA. After the COVID-19 pandemic, even more people obtained a life insurance policy, which increased mortality risk for insurance providers.

To be successful in the very competitive insurance coverage trade, firms need to take care of risk and get ready for the future. While it's impossible to forecast the future with assurance, every insurance company will understand that it is necessary to prepare exhaustively. This is where an actuarial professional can enter into play. Anticipating modeling and data analytics can help establish expectations.

Are you still not sure where to begin with an actuary? Do not fret, Lewis & Ellis are right here to lead you and the insurance provider through the procedure. We have developed a collection of Windows-based actuarial software program to assist our professionals and outside actuaries in effectively and properly completing most of their tasks.

{kind=link}

Latest Posts

Mortality Charge For Universal Life Policies

Best Variable Universal Life Insurance Policy

Maximum Funded Tax Advantaged Insurance Contracts